by Pratik Datta and Chirag Anand.

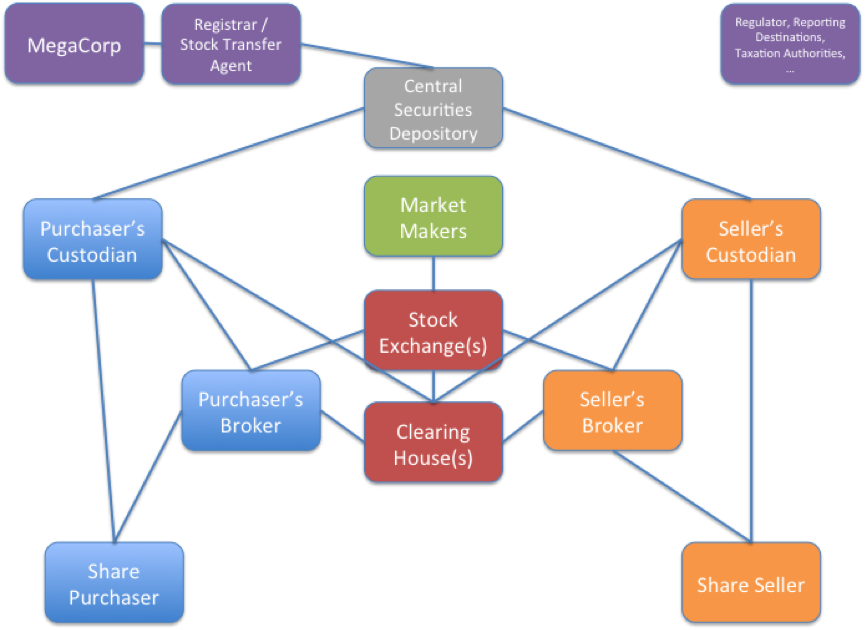

In a modern securities market, eight different entities are involved in trading a single security: Two brokers, two custodians, a stock exchange, a clearing house, a central securities depository, and a registrar or stock transfer agent. The image below shows the working connections among these entities while trading the securites of MegaCorp, a hypothetical company. The entire process is very well articulated here. This complex institutional machinery delivers low transactions costs. For a contrast, transactions costs are much higher in the Indian Bond-Currency-Derivatives Nexus, which has not achieved such sophisticated institutional arrangements.

As shown in the image, the client instructs its broker to place an order to buy or sell a security. Such orders can be of two types:

Market orders: An order to buy or sell securities at the best price obtainable after entering the system.

Limit orders: An order that allows the price to be specified before entering the system.

On instructions from the client, the broker executes the instruction by keying the order (to sell or to buy) into the system. The moment the order hits the server, matching happens, followed by clearing and settlement. But to err is human and brokers are no exceptions. The world over, there have been incidents of brokers keying in incorrect orders by mistake leading to erroneous trades. Such erroneous trades are referred to as "fat finger trades". The worst fat finger trades are the ones where a huge order is placed by mistake, triggering a chain reaction of price fluctuations in the security across the market leading to a flash crash.

Given that fat finger trades may be disruptive (although unintentional), there are two schools of thought about what should be done about them. One school argues that such trades, being erroneous, should be cancelled. The other school is of the view that allowing cancellation is akin to bailing out the negligent broker who committed the error. Cancelling such erroneous trades will lead to moral hazard issues - brokers will have no incentive to be careful while placing orders, they will not develop better software to prevent such errors in future. Further, there is the complexity of undoing transactions involving multiple entities as shown in the image above. So, instead of cancelling the trades, it is better to impose pecuniary penalties on the wrong-doers and compensate the aggrieved persons.

Under the present Indian laws, exchanges have the discretion to annul fat finger trades on a case to case basis. This position is problematic from a policy perspective as is argued below.

In this backdrop, the Securities Appellate Tribunal's decision last week in M/s. Emkay Global Financial Services Ltd. v. NSE, directing NSE to consider afresh whether trades executed between Emkay and two of the respondents should be annulled (at paragraph 42), assumes special significance.

SAT: Left this issue open for NSE to re-consider after hearing the concerned parties. [See paragraph 42]

Reasons: NSE in its circular dated January 20, 2004, requested its members to refrain from placing orders at unrealistic prices which are far away from the normal market price/theoretical price at that point of time since it affects the normal price discovery process. Respondents 2 and 3 had placed limit orders to buy at a price lower than the market price. The moment the fat finger sell order was placed from Emkay's end, the prices plummeted till they finally matched the pre-placed limit order price of Respondents 2 and 3. In the process, Emkay lost out on a lot of money while Respondents 2 and 3 made a huge profit. Later, one of the grounds on which Emkay asked NSE to annul the trades was that Respondents 2 and 3 had placed unrealistic buy orders far away from the market price in breach of the NSE circular dated January 20, 2004. Had such orders not been placed illegally, Emkay's fat finger trade market order to sell would not have found a match and would not have been executed. That would have given Emkay the opportunity to cancel the erroneous order. NSE rejected this argument on the following grounds:

SAT did not agree with this aspect of NSE's order for the following reasons:

Accordingly, SAT directed NSE to reconsider the matter after hearing the parties afresh. Moreover, it clarified that NSE will decide whether it would be just and proper to annul or some of the trades executed between Emkay and Respondents 2 and 3.

We think that on issues (1) and (2), SAT rightly rejected Emkay's plea of annulment. However, its decision in (3) to remand the matter back to NSE for reconsideration, keeping the option of annulment open, was unnecessary and undesirable from a policy level.

SAT presumed that limit orders which are far away from the market price are undesirable. This presumption was based on NSE circulars dated January 20, 2004 and February 22, 2005. Curiously, both these circulars are applicable to the derivatives segment and not to the NIFTY 50 scrips in question, which took place on the equity segment. Moreover, these circulars do not specify any price band within which limit orders should be placed. It is entirely up to the exchange to decide on a case to case basis whether a limit order has detrimentally impacted the price discovery process and accordingly if disciplinary action should be taken. In this case, SAT did not cite any such action by NSE against Respondents 2 and 3.

Further, limit orders for NIFTY 50 scrips were not subject to any price band at the time of the fat finger trade on October 5, 2012. The SEBI circular dated June 28, 2001, required individual scrip wise price bands of 20% either way. But this circular did not extended to scrips on which derivative products were available or scrips included in indices on which derivatives products were available. Clearly NIFTY 50 scrips were excluded from the scope of this circular. Subsequently, only after the Emkay fat finger trade incident, SEBI issued a circular on December 13, 2012, imposing dynamic price bands of 10% of the previous closing price on stocks included in indices on which derivatives products are available and stocks on which derivatives products are available. NSE issued circular number 78/2012 (download ref. no. NSE/SURV/22310) on December 14, 2012, taking note of the SEBI circular dated December 13, 2012. On December 17, 2012, NSE issued another circular bearing number 80/2012 (download ref. no. NSE/CMTR/22322) stating that the dynamic price bands shall be 10% for stocks on which derivatives products are available and stocks included in indices on which derivatives products are available. Members were advised not to place orders beyond the dynamic price bands in force. Consequently, placing limit orders on NIFTY 50 scrips at a price beyond 10% of the last traded price was made illegal only after December 17, 2012.

Therefore, on October 5, 2012, Respondents 2 and 3 did not violate any law in force on that date when their limit orders on NIFTY 50 scrips were executed at a price around 20% away from the market price. It would be unjust and illegal to apply the NSE circular dated December 17, 2012, retrospectively to penalise them. Further, in absence of any specific steps by NSE against Respondents 2 and 3 on the limit order issue, SAT had no reason to presume that the limit orders placed by Respondents 2 and 3 were undesirable. In fact, to the contrary, limit orders may play a crucial stabilisation role in extremely volatile situations by acting as a safety net.

From the viewpoint of the basic economics, limit orders far away from the touch stabilise the market and should be welcome. There is absolutely no market failure when limit orders are placed far away from the touch and there is no case for using the coercive power of the State in interfering with these private choices.

SAT's final directions to NSE give the impression that violation of margin money can be remedied by annulment of trades. This is akin to missing the forest for the trees. In organised financial trading, a member is required to provide margin money to protect the counterparties from it's credit risk. Over and above margin money requirement, a central counterparty is inserted in the transaction to further protect the counterparties from the member's credit risk. Both margin money and a central counterparty are means to an end - the end being finality of a trade once executed. Therefore, annulling the trade itself for violation of the margin money norms would defeat the broader purpose of having a margin money requirement in the first place. Consequently, even if Respondents 2 and 3 violated the margin money norms, the remedy is not to annul the trades in which they were counterparties. Therefore, SAT should not have left the option of annulment open for reconsideration by NSE. Adequate pecuniary penalties on Respondents 2 and 3 would serve the purpose.

Emkay argued that since the fat finger trade was executed due to a mistake, the contract itself was void under the Indian Contract Act, 1872. Mr. A.S. Lamba, a SAT member, rejected this argument (in paragraph 27) on the ground that `Contract Act cannot be imported to present case, since laws governed securities market are adequate to deal with the present case and Contract Act, 1872 came into existence, when present day securities market did not exist or were even contemplated'. This reasoning, based on the principle of contemporanea expositio, is contrary to the Supreme Court judgement in Senior Electricity Inspector v. Laxmi Narayan Chopra, AIR 1962 SC 159, which held:

This judgment gives us an occassion to rethink the policy behind annulment of fat finger trades and accordingly, how to rewrite the laws and regulations sarrounding it. We would suggest there are three key ideas:

Finality of the trade. When an investor sells or buys a security, she expects to receive the assured sum of money or the securities as promised. This is the basic objective of the trade. If the organised financial trading system fails to assure the investor of this basic objective, investors will lose confidence in the securities market. This is the reason why central counterparties were introduced to insulate each member from the counterparty's credit risk. To boost investor confidence, finality of settlement has been recognised in most jurisdictions. IOSCO also requires clear legal basis for settlement finality.

In India, the Payments and Settlements Systems Act, 2007 recognises `netting' and also makes `settlement' final and irrevocable. However, this Act does not extend to stock exchanges and clearing corporations. Consequently, netting and settlement done by stock exchanges or clearing corporations is not treated as final and irrevocable under any statutory law. Instead, finality of settlement in the Indian context is embedded in the bye-laws of the exchanges only. This legal position is undesirable since bye-laws of the exchange can be overridden by other statutory laws (like Companies Act, 2013 during winding up).

The Financial Sector Legislative Reforms Commission (FSLRC) noted that transactions on an Infrastructure Institution cannot be easily undone. In netting and settling systems, if any individual transaction is undone, all dependant transactions will also have to be undone. This would create uncertainty for all persons using such institutions. Failure of a transaction in the exchange may have domino effect on other transactions. Therefore, the FSLRC categorically recommended that transactions on an Infrastructure Institution should be final and not undone under any circumstances. Instead, it favours pecuniary compensation for the aggrieved party.

Exchanges should not be given vague powers. Under the present arrangements, a trade can be annulled by the stock exchange under its bye-laws. These clauses, like Cl. 5(a), NSE Byelaws, do not provide any principle on the basis of which the exchange will annul a trade. It is completely up to the subjective satisfaction of the exchange. This is bad legal drafting. Besides being a clear indication of lack of basic policy thinking, it also opens up the possibilities of regulatory capture - a dominant group of traders may unduly benefit from this system. For example, Prof. Varma expressed his apprehension that SEC's 2009 move to annul trades that deviate substantially from current market prices may be the consequence of regulatory capture.

Understanding the market failure and addressing it directly. When person X engages in a fat finger trade, for a brief time he distorts the price and liquidity of the market. This imposes externalities upon others. There is a market failure here.

Financial firms and traders have an incentive to underinvest in building high quality software systems as they do not bear the full consequences of their actions.

Hence, the framework of policy should be designed in a way that makes it very painful for financial firms to make mistakes. See SEBI's recent endeavour to rethink the policy underlying annulment of fat finger trades, and the analysis of this by Finance Research Group at IGIDR.

Annulling fat finger trades is a bad idea because:

Moral hazard on low quality software systems: Annuling a trade done by a trader negligently ensures that the trader will never mend his ways in the future. He knows that his negligence will always be excused and never cause him any harm.

Incentives for stabilising strategies: Two types of trading strategies help check extreme price movements caused due to a fat finger trade. First, limit orders placed far away from the normal market price; second, arbitrageurs who take opposite position realising that its a temporary error.

Moral hazard on trading strategies: It is impossible for the exchange to determine if a fat finger trade was due to genuine mistake or deliberate plan. Once the law mandates that fat finger trades will be annulled, rogue traders may take advantage of that rule to enter into trades and get them cancelled subsequently. In the process, they may make illicit profits at the cost of the other genuine market participants.

SEBI's initiative to rethink the philosophy behind annulment of fat finger trades is a positive sign. SEBI should take this opportunity to implement the FSLRC proposal and prohibit exchanges from annulling fat finger trades. Instead of undoing trade finality, it would be far easier and desirable to ameliorate hardships through pecuniary compensations.

In a modern securities market, eight different entities are involved in trading a single security: Two brokers, two custodians, a stock exchange, a clearing house, a central securities depository, and a registrar or stock transfer agent. The image below shows the working connections among these entities while trading the securites of MegaCorp, a hypothetical company. The entire process is very well articulated here. This complex institutional machinery delivers low transactions costs. For a contrast, transactions costs are much higher in the Indian Bond-Currency-Derivatives Nexus, which has not achieved such sophisticated institutional arrangements.

{kind=link}

As shown in the image, the client instructs its broker to place an order to buy or sell a security. Such orders can be of two types:

On instructions from the client, the broker executes the instruction by keying the order (to sell or to buy) into the system. The moment the order hits the server, matching happens, followed by clearing and settlement. But to err is human and brokers are no exceptions. The world over, there have been incidents of brokers keying in incorrect orders by mistake leading to erroneous trades. Such erroneous trades are referred to as "fat finger trades". The worst fat finger trades are the ones where a huge order is placed by mistake, triggering a chain reaction of price fluctuations in the security across the market leading to a flash crash.

Given that fat finger trades may be disruptive (although unintentional), there are two schools of thought about what should be done about them. One school argues that such trades, being erroneous, should be cancelled. The other school is of the view that allowing cancellation is akin to bailing out the negligent broker who committed the error. Cancelling such erroneous trades will lead to moral hazard issues - brokers will have no incentive to be careful while placing orders, they will not develop better software to prevent such errors in future. Further, there is the complexity of undoing transactions involving multiple entities as shown in the image above. So, instead of cancelling the trades, it is better to impose pecuniary penalties on the wrong-doers and compensate the aggrieved persons.

Under the present Indian laws, exchanges have the discretion to annul fat finger trades on a case to case basis. This position is problematic from a policy perspective as is argued below.

In this backdrop, the Securities Appellate Tribunal's decision last week in M/s. Emkay Global Financial Services Ltd. v. NSE, directing NSE to consider afresh whether trades executed between Emkay and two of the respondents should be annulled (at paragraph 42), assumes special significance.

Emkay v. NSE: Facts

- On October 5, 2012, Emkay's trader punched an order to sell 17 lakh NIFTY 50 units instead of punching order to sell Rs.17 lakh worth of NIFTY 50 units.

- The sell orders in (1) culminated into a transaction because Respondents 2 to 9 placed unrealistic buy orders to buy NIFTY 50 stocks at prices far away from the market price, without adequate margin money.

- As per SEBI's circular, the index-based market wide circuit breaker system of NSE ought to have brought about a coordinated trading halt when the NIFTY index fell below 10%. However, in this case, NSE's circuit breaker did not halt when NIFTY index fell below 10%. It halted only when the NIFTY index fell by 15.5%.

- NSE allowed trading to resume within 15 minutes of the halt, in violation of a SEBI circular.

- NSE did not agree with the Emkay's plea to annul the trades on the ground that there was "material mistake in the trade" under Cl. 5(a), NSE Byelaws.

Legal issues addressed by SAT

- Whether the `material mistake' clause in Cl. 5(a), NSE Byelaws is intended to protect fat finger traders?

SAT: No.

Reason: Emkay was found guilty of committing breach of duty by not installing a suitable validation mechanism before entering a sell order. It was also guilty of negligently transmitting an erroneous sell order from the dealer's terminal to the NSE's server by ignoring four to five level checks that were available in the system. SAT held that Cl. 5(a) is not intended to give relief to a trader who is guilty of not exercising due care and caution and is guilty of negligence. [See paragraph 20]

- Whether a fat finger trade should be annulled because of violation of margin money requirements by the trader?

SAT: No.

Reason: Annulling trades at the instance of trading members who are guilty of violating margin money norms would be unjustified as it would virtually amount to permitting trading members to trade by violating margin money norms and seek annulment wherever the trades are adverse to the interest of the trading members. In such a case annulment of trades would amount to frustrating the objects with which margin money norms have been framed. [See paragraph 28]

- Whether a stock exchange can refuse to annul a fat finger trade on the ground of material mistake in the trade when both parties to the trade are guilty of violating the norms?

SAT: Left this issue open for NSE to re-consider after hearing the concerned parties. [See paragraph 42]

Reasons: NSE in its circular dated January 20, 2004, requested its members to refrain from placing orders at unrealistic prices which are far away from the normal market price/theoretical price at that point of time since it affects the normal price discovery process. Respondents 2 and 3 had placed limit orders to buy at a price lower than the market price. The moment the fat finger sell order was placed from Emkay's end, the prices plummeted till they finally matched the pre-placed limit order price of Respondents 2 and 3. In the process, Emkay lost out on a lot of money while Respondents 2 and 3 made a huge profit. Later, one of the grounds on which Emkay asked NSE to annul the trades was that Respondents 2 and 3 had placed unrealistic buy orders far away from the market price in breach of the NSE circular dated January 20, 2004. Had such orders not been placed illegally, Emkay's fat finger trade market order to sell would not have found a match and would not have been executed. That would have given Emkay the opportunity to cancel the erroneous order. NSE rejected this argument on the following grounds:

- in an anonymous trading system counter parties do not know who is on the other side and their intention of placing buy or sell orders;

- the buy orders of Respondents 2 and 3 were already there in the system before Emkay placed the fat finger order;

- unlawful gains by Respondents 2 and 3 were not germane to the issue under consideration.

SAT did not agree with this aspect of NSE's order for the following reasons:

- NIFTY index fell by 15.5% because of this fat finger trade. Consequently, trading had to be temporarily halted;

- More stringent actions should have been taken against Respondents 2 and 3 for regularly placing orders far away from market price;

- Penalty of Rs. 20-25 lakhs on Respondents 2 and 3 is inadequate in light of the profits made by them in this case.

Accordingly, SAT directed NSE to reconsider the matter after hearing the parties afresh. Moreover, it clarified that NSE will decide whether it would be just and proper to annul or some of the trades executed between Emkay and Respondents 2 and 3.

We think that on issues (1) and (2), SAT rightly rejected Emkay's plea of annulment. However, its decision in (3) to remand the matter back to NSE for reconsideration, keeping the option of annulment open, was unnecessary and undesirable from a policy level.

Applicability of NSE circulars

SAT presumed that limit orders which are far away from the market price are undesirable. This presumption was based on NSE circulars dated January 20, 2004 and February 22, 2005. Curiously, both these circulars are applicable to the derivatives segment and not to the NIFTY 50 scrips in question, which took place on the equity segment. Moreover, these circulars do not specify any price band within which limit orders should be placed. It is entirely up to the exchange to decide on a case to case basis whether a limit order has detrimentally impacted the price discovery process and accordingly if disciplinary action should be taken. In this case, SAT did not cite any such action by NSE against Respondents 2 and 3.

Further, limit orders for NIFTY 50 scrips were not subject to any price band at the time of the fat finger trade on October 5, 2012. The SEBI circular dated June 28, 2001, required individual scrip wise price bands of 20% either way. But this circular did not extended to scrips on which derivative products were available or scrips included in indices on which derivatives products were available. Clearly NIFTY 50 scrips were excluded from the scope of this circular. Subsequently, only after the Emkay fat finger trade incident, SEBI issued a circular on December 13, 2012, imposing dynamic price bands of 10% of the previous closing price on stocks included in indices on which derivatives products are available and stocks on which derivatives products are available. NSE issued circular number 78/2012 (download ref. no. NSE/SURV/22310) on December 14, 2012, taking note of the SEBI circular dated December 13, 2012. On December 17, 2012, NSE issued another circular bearing number 80/2012 (download ref. no. NSE/CMTR/22322) stating that the dynamic price bands shall be 10% for stocks on which derivatives products are available and stocks included in indices on which derivatives products are available. Members were advised not to place orders beyond the dynamic price bands in force. Consequently, placing limit orders on NIFTY 50 scrips at a price beyond 10% of the last traded price was made illegal only after December 17, 2012.

Therefore, on October 5, 2012, Respondents 2 and 3 did not violate any law in force on that date when their limit orders on NIFTY 50 scrips were executed at a price around 20% away from the market price. It would be unjust and illegal to apply the NSE circular dated December 17, 2012, retrospectively to penalise them. Further, in absence of any specific steps by NSE against Respondents 2 and 3 on the limit order issue, SAT had no reason to presume that the limit orders placed by Respondents 2 and 3 were undesirable. In fact, to the contrary, limit orders may play a crucial stabilisation role in extremely volatile situations by acting as a safety net.

From the viewpoint of the basic economics, limit orders far away from the touch stabilise the market and should be welcome. There is absolutely no market failure when limit orders are placed far away from the touch and there is no case for using the coercive power of the State in interfering with these private choices.

Margin money

SAT's final directions to NSE give the impression that violation of margin money can be remedied by annulment of trades. This is akin to missing the forest for the trees. In organised financial trading, a member is required to provide margin money to protect the counterparties from it's credit risk. Over and above margin money requirement, a central counterparty is inserted in the transaction to further protect the counterparties from the member's credit risk. Both margin money and a central counterparty are means to an end - the end being finality of a trade once executed. Therefore, annulling the trade itself for violation of the margin money norms would defeat the broader purpose of having a margin money requirement in the first place. Consequently, even if Respondents 2 and 3 violated the margin money norms, the remedy is not to annul the trades in which they were counterparties. Therefore, SAT should not have left the option of annulment open for reconsideration by NSE. Adequate pecuniary penalties on Respondents 2 and 3 would serve the purpose.

Applicability of Contract Act, 1872

Emkay argued that since the fat finger trade was executed due to a mistake, the contract itself was void under the Indian Contract Act, 1872. Mr. A.S. Lamba, a SAT member, rejected this argument (in paragraph 27) on the ground that `Contract Act cannot be imported to present case, since laws governed securities market are adequate to deal with the present case and Contract Act, 1872 came into existence, when present day securities market did not exist or were even contemplated'. This reasoning, based on the principle of contemporanea expositio, is contrary to the Supreme Court judgement in Senior Electricity Inspector v. Laxmi Narayan Chopra, AIR 1962 SC 159, which held:

...in a modern progressive society it would be unreasonable to confine the intention of a Legislature to the meaning attributable to the word used at the time the law was made, for a modern Legislature making laws to govern a society which is fast moving must be presumed to be aware of an enlarged meaning the same concept might attract with the march of time and with the revolutionary changes brought about in social, economic, political and scientific and other fields of human activity. Indeed, unless a contrary intention appears, an interpretation should be given to the words used to take in new facts and situations, if the words are capable of comprehending them.Although SAT was correct in rejecting Emkay's argument based on mistake, SAT's blanket reasoning that Indian Contract Act, 1872, does not apply to transactions in securities is incorrect. Instead, it should have read in Regulation 6A(1)(b) of SEBI (Stock brokers and sub-brokers) Regulations, 1992 and Cl. 5(a), NSE Byelaws while interpreting the contract between NSE and Emkay to refute this argument.

How to think about trade annulment

This judgment gives us an occassion to rethink the policy behind annulment of fat finger trades and accordingly, how to rewrite the laws and regulations sarrounding it. We would suggest there are three key ideas:

- Finality of the trade.

- Exchanges should not be given vague powers

- The market failure and how to address it.

Finality of the trade. When an investor sells or buys a security, she expects to receive the assured sum of money or the securities as promised. This is the basic objective of the trade. If the organised financial trading system fails to assure the investor of this basic objective, investors will lose confidence in the securities market. This is the reason why central counterparties were introduced to insulate each member from the counterparty's credit risk. To boost investor confidence, finality of settlement has been recognised in most jurisdictions. IOSCO also requires clear legal basis for settlement finality.

In India, the Payments and Settlements Systems Act, 2007 recognises `netting' and also makes `settlement' final and irrevocable. However, this Act does not extend to stock exchanges and clearing corporations. Consequently, netting and settlement done by stock exchanges or clearing corporations is not treated as final and irrevocable under any statutory law. Instead, finality of settlement in the Indian context is embedded in the bye-laws of the exchanges only. This legal position is undesirable since bye-laws of the exchange can be overridden by other statutory laws (like Companies Act, 2013 during winding up).

The Financial Sector Legislative Reforms Commission (FSLRC) noted that transactions on an Infrastructure Institution cannot be easily undone. In netting and settling systems, if any individual transaction is undone, all dependant transactions will also have to be undone. This would create uncertainty for all persons using such institutions. Failure of a transaction in the exchange may have domino effect on other transactions. Therefore, the FSLRC categorically recommended that transactions on an Infrastructure Institution should be final and not undone under any circumstances. Instead, it favours pecuniary compensation for the aggrieved party.

Exchanges should not be given vague powers. Under the present arrangements, a trade can be annulled by the stock exchange under its bye-laws. These clauses, like Cl. 5(a), NSE Byelaws, do not provide any principle on the basis of which the exchange will annul a trade. It is completely up to the subjective satisfaction of the exchange. This is bad legal drafting. Besides being a clear indication of lack of basic policy thinking, it also opens up the possibilities of regulatory capture - a dominant group of traders may unduly benefit from this system. For example, Prof. Varma expressed his apprehension that SEC's 2009 move to annul trades that deviate substantially from current market prices may be the consequence of regulatory capture.

Understanding the market failure and addressing it directly. When person X engages in a fat finger trade, for a brief time he distorts the price and liquidity of the market. This imposes externalities upon others. There is a market failure here.

Financial firms and traders have an incentive to underinvest in building high quality software systems as they do not bear the full consequences of their actions.

Hence, the framework of policy should be designed in a way that makes it very painful for financial firms to make mistakes. See SEBI's recent endeavour to rethink the policy underlying annulment of fat finger trades, and the analysis of this by Finance Research Group at IGIDR.

Annulling fat finger trades is a bad idea because:

SEBI's initiative to rethink the philosophy behind annulment of fat finger trades is a positive sign. SEBI should take this opportunity to implement the FSLRC proposal and prohibit exchanges from annulling fat finger trades. Instead of undoing trade finality, it would be far easier and desirable to ameliorate hardships through pecuniary compensations.

The legal framework for strengthening finality of settlement and netting was done in Sept 2013. the link is http://www.sebi.gov.in/cms/sebi_data/attachdocs/1378378058586.pdf. This is better than the earlier situation of languishing only in the bye-laws of the Clearing Corporation and less than putting it in the SCRA. Regulation is deemed passed by Parliament .

ReplyDeleteDear Siva,

DeleteThanks for sharing your thoughts. Regulations passed by SEBI under section 30 are laid before the Parliament vide section 31, SEBI Act, 1992. However, this does not make it akin to a statute enacted by Parliament (like Companies Act, 2013). In case of a conflict between any statutory law and a SEBI regulation, the statute will override the regulation. Given that Indian statutes use non-obstante clauses quite generously, the only solution would be to have settlement finality of securities transactions protected by a Parliamentary statute (like PSS Act 2007) and not merely through SEBI regulations or exchange bye-laws.

Pratik.