We are all used to seeing the options chain for Nifty, but now you have one for INR/USD.

Also read Mobis Philipose in Mint on the unfinished business of derivatives trading in India.

Friday, October 29, 2010

Who will make the exchange-traded currency options market?

In a few minutes, NSE and USE will start trading in currency options. This will be the first exchange-traded options in India on a non-equity underlying.

Currency options are obviously useful as a risk-management tool. I feel that futures are nice simple linear contracts: they ask the person to make only one decision -- are you long or are you short. But once a futures position is entered into, the person needs the ability to manage the position since daily marking-to-market is done, and since there can be large losses for either the futures long or the futures short.

Compared with this, long positions on call or put options appeal to the kind of person that is willing to think carefully about a position at the outset, but after that it is fire and forget. This better describes the life of many firms exposed to currency risk, particularly those with relatively weak treasuries.

Currency options have, of course, been traded OTC for some time now. But there are real problems with this market. Customers have sometimes been ripped off by banks on pricing, given the lack of a liquid and transparent comparison point. While currency options are offered by banks to customers, there is not much by way of an inter-bank market.

As far as I know, there is relatively little by way of a build-up of human and systems capability in the banks for currency options trading (whether OTC or on exchange).

In contrast, there is a remarkable build-up of human and systems capability in the world of Nifty options trading. Options on Nifty have shaped up as one of the biggest options markets in the world. This involves end-users who think and trade options, staff working for securities firms who understand options (and understand issues about their credit risk when their customer has an options position), analytical software systems, and (most importantly) algorithmic trading systems. Options trading inevitably involves trading in a large number of underlyings. Strong computer systems which are able to think about, and place orders in, all the underlyings at one shot are of essence in achieving option liquidity. Such capabilities are now found in the world of Nifty options, and are absent in banks or in the OTC currency options market.

It is fairly easy for a person trading Nifty options to move to trading currency options. Hence, the brainpower and systems that have made Nifty options one of the world's top contracts will easily be able to move to currency options trading, and make it work. I expect that the securities firms who dominate Nifty options trading will now dominate currency options trading.

I think three kinds of stories will now kick in:

Currency options are obviously useful as a risk-management tool. I feel that futures are nice simple linear contracts: they ask the person to make only one decision -- are you long or are you short. But once a futures position is entered into, the person needs the ability to manage the position since daily marking-to-market is done, and since there can be large losses for either the futures long or the futures short.

Compared with this, long positions on call or put options appeal to the kind of person that is willing to think carefully about a position at the outset, but after that it is fire and forget. This better describes the life of many firms exposed to currency risk, particularly those with relatively weak treasuries.

Currency options have, of course, been traded OTC for some time now. But there are real problems with this market. Customers have sometimes been ripped off by banks on pricing, given the lack of a liquid and transparent comparison point. While currency options are offered by banks to customers, there is not much by way of an inter-bank market.

As far as I know, there is relatively little by way of a build-up of human and systems capability in the banks for currency options trading (whether OTC or on exchange).

In contrast, there is a remarkable build-up of human and systems capability in the world of Nifty options trading. Options on Nifty have shaped up as one of the biggest options markets in the world. This involves end-users who think and trade options, staff working for securities firms who understand options (and understand issues about their credit risk when their customer has an options position), analytical software systems, and (most importantly) algorithmic trading systems. Options trading inevitably involves trading in a large number of underlyings. Strong computer systems which are able to think about, and place orders in, all the underlyings at one shot are of essence in achieving option liquidity. Such capabilities are now found in the world of Nifty options, and are absent in banks or in the OTC currency options market.

It is fairly easy for a person trading Nifty options to move to trading currency options. Hence, the brainpower and systems that have made Nifty options one of the world's top contracts will easily be able to move to currency options trading, and make it work. I expect that the securities firms who dominate Nifty options trading will now dominate currency options trading.

I think three kinds of stories will now kick in:

- Liquidity in currency options will fuel liquidity in currency futures, and vice versa. Corporate hedgers will be more interested in either, given that the other is also a possibility.

- Skills and systems from Nifty options will flow into currency options. Banks will be able to rapidly bulk up their options capabilities by recruiting from the world of Nifty options, and by purchasing the software systems that have sprung up in that space.

- Conversely, trading in both currency options and Nifty options will generate an increased business size for people who build knowledge and systems for options; it will also improve knowledge of options trading through an understanding and comparison of the nuances of two different underlyings. The number of FRM and PRM certified people in India will go up.

Of great interest will be the question of currency volatility. On one hand, the currency options market will generate an implied volatility for the currency, which will represent a market-based forecast for what future currency vol will be. This will be a big new piece of information which will inform macro policy and monetary policy, and thus diminish the extent to which we are flying blind in thinking about Indian macroeconomics.

In recent years, RBI has mostly stayed off from trading the currency market, so the volatility of the INR/USD is a true market volatility. If, in the future, RBI thinks that it wants to give subsidised currency risk management services to the private sector, one way in which it would be able to do that is to do `intervention' on the currency options market so as to force down the implied vol of the market. I.e., RBI would sell ATM calls and ATM puts and thus drive down that price, and thus give cheaper risk management services to the market. This would represent the first operational intervention strategy for RBI through which it can pursue the goal of reducing volatility without distorting the INR/USD exchange rate.

If RBI gets into actively trading the currency market again and trying to push the rupee into a de facto pegged exchange rate, we will see this clearly in the currency options market as a sharply reduced implied vol.

Tuesday, October 26, 2010

Better living through economics

The `lemons model' in milk procurement

One of the classic stories of India of old is that of Amul, which brought new technology into milk procurement. When the farmer brought his shipment of milk to the Amul front-end, a centrifuge was used to measure the characteristics of this shipment, and based on this payments were made. See this blog post by Alok Parekh, Naman Pugalia and Mihir Sheth. This eliminated the incentives for aduleration of milk by the farmer, which used to be done by adding in water or by skimming the cream.

We can think about this differently. Suppose the centrifuge was not there at the front end. Then the buyer of the milk faced asymmetric information about the characteristics of the milk that were being offered to him. Generally we expect that faced with this `lemons' problem, the buyer would bid low prices for the milk.

So to some extent, the ability of Amul to pay higher prices for milk is not about the greatness of cooperatives when compared with profit-oriented firms: it was about the injection of new technology which removed this asymmetric information.

The interesting puzzle is: in that age, why was Amul the pioneer in buying centrifuges? Why did no private firm buy centrifuges and create a winning business model around milk?

Penalty structure under incomplete detection

Another nice idea that we have understood is the relationship between the probability of getting caught and the penalty. Suppose the fee required for parking is Rs.10 and suppose the probability of getting caught when illegally parked (i.e. without paying the fee) is 10%. Then it's sensible to set the penalty for getting caught at Rs.100 so that even a risk-neutral person will prefer to play by the rules.

This can be applied in the problem of milk procurement. Suppose we say to the farmer: We'll trust you and accept your milk, but on a sampling basis, one in ten farmers will be tested.

Suppose a person added 2 litres of water to his shipment of milk and suppose the price of milk was Rs.10 a litre. In that case, he was trying to steal Rs.20 by palming off low quality milk. But there was only a 10% probability of getting caught, because only one in ten farmers is tested. So the penalty he should face should be Rs.200. If this is done, the risk-neutral farmer is agnostic between playing fair and cheating, even if only one in ten farmers is tested.

The advantage of this strategy is that for 90% of the farmers, the deadweight cost of putting a sample into the centrifuge is eliminated.

This idea is, of course, general:

- Sometimes, we are in situations (as in market manipulation in finance) where we know that even the best regulator in the world will only catch some of the crooks. So we should estimate what fraction of the crooks are getting caught, and then multiply up the size of theft that was attempted. That is, the right way to think of disgorgement is not that the bad guys should fork up the money that was stolen, but that the penalty imposed by the government should be equal to the size of theft divided by the probability of detection.

- Sometimes, while comprehensive checking is feasible, it's quite expensive, and it's efficient to deliberately only do checking on a sampling basis. A fairly modest scale of randomised checking (e.g. 5%) can do the trick, coupled with a 20x multiplication factor against the size of the theft that was attempted. This would yield a 95% reduction in the amount of checking that is required. This is the idea in the milk example above.

A cross-country comparison of charges of exchanges

In reading this article in the Wall Street Journal by By Rebecca Thurlow, Alison Tudor And P. R. Venkat about the potential merger of SGX with ASX, I saw this interesting cross-country comparison of exchange charges (in basis points):

It is quite a striking set of facts.

First, we see that in terms of the core trading and clearing -- the charges of the exchange -- India is the 2nd lowest in this pile, with a value of 0.35 basis points. This is slightly worse than Japan (0.24 basis points) and superior to all the others. This partly derives from the immense economies of scale at NSE and BSE, which are ranked at 3 and 5 in the world by number of transactions. This is also about the cost-efficiency of the human part of running an exchange: small exchanges like SGX cannot match the price points which NSE and BSE can reach. In this field, as in finance more broadly, India is pretty good at reaching up to world class at below the world price. This was the basic logic, if you recall, of Percy Mistry's Mumbai as an International Financial Centre report.

Secondly, we see the huge problem that transactions taxes present in all these countries other than Singapore, Australia and Japan. The Indian charge of 0.35 basis points is just swamped by the taxation of 27 basis points. Even if NSE cut charges by half, and got down to 0.175 basis points, this would do nothing for the end-customer who is paying 27.35 today and ends up paying 27.175 across the price cut. Conversely, Singapore, with the least efficient exchange (4.75 basis points) ends up being a nice place for the customer because there is no tax upon transactions there: only Australia and Japan are better than Singapore.

Economists are very clear that all taxation of transactions is distortionary. It's puzzling why so many countries (four out of these seven) continue to indulge in something which is an elementary mistake in public policy.

| Country | Trading and clearing | Taxes |

| Singapore | 4.75 | 0 |

| Hong Kong | 1.1 | 20 |

| Taiwan | 0.75 | 30 |

| Korea | 0.54 | 30 |

| Australia | 0.53 | 0 |

| India | 0.35 | 27 |

| Japan | 0.24 | 0 |

It is quite a striking set of facts.

First, we see that in terms of the core trading and clearing -- the charges of the exchange -- India is the 2nd lowest in this pile, with a value of 0.35 basis points. This is slightly worse than Japan (0.24 basis points) and superior to all the others. This partly derives from the immense economies of scale at NSE and BSE, which are ranked at 3 and 5 in the world by number of transactions. This is also about the cost-efficiency of the human part of running an exchange: small exchanges like SGX cannot match the price points which NSE and BSE can reach. In this field, as in finance more broadly, India is pretty good at reaching up to world class at below the world price. This was the basic logic, if you recall, of Percy Mistry's Mumbai as an International Financial Centre report.

Secondly, we see the huge problem that transactions taxes present in all these countries other than Singapore, Australia and Japan. The Indian charge of 0.35 basis points is just swamped by the taxation of 27 basis points. Even if NSE cut charges by half, and got down to 0.175 basis points, this would do nothing for the end-customer who is paying 27.35 today and ends up paying 27.175 across the price cut. Conversely, Singapore, with the least efficient exchange (4.75 basis points) ends up being a nice place for the customer because there is no tax upon transactions there: only Australia and Japan are better than Singapore.

Economists are very clear that all taxation of transactions is distortionary. It's puzzling why so many countries (four out of these seven) continue to indulge in something which is an elementary mistake in public policy.

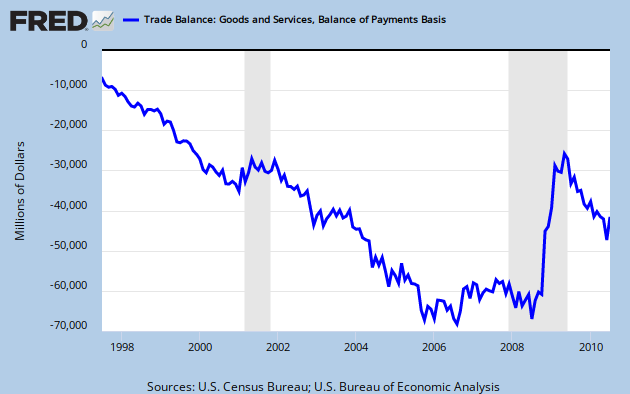

Wednesday, October 13, 2010

Currency conflicts come to prominence again

From the mid 1990s onwards, the US trade balance has steadily become bigger. This is a centrepiece of the problem of `global imbalances'. Starting from values of roughly zero, this got all the way to values like $70 billion a month, where the US was importing over $2 billion a day of capital to pay for the trade deficit. Here's the picture:

This was termed as the `Bretton Woods II' configuration, where exporting countries like China gave loans to the US, in a form of suppliers' credit, and the US bought Chinese goods. This magnitude of capital import was un-sustainable for the US. Something had to give.

|

| The US trade balance (goods+services, per month, seasonally adjusted) |

Warning for Indian readers: In India, the term `trade balance' pertains only to merchandise trade. In the US, the monthly trade data covers both goods and services. So it is a meaningful measure of what is going on in international trade, unlike the corresponding Indian data.

Bretton Woods II first broke down in the financial crisis. In the downturn, the mighty American consumer purchased fewer 50" television sets. The US trade deficit dropped nicely all the way to $25 billion per month. Alongside a rise in the US savings rate, this looked like a world which was rebalancing.

In recent months, this movement reversed itself and the US trade deficit once again started getting worse. A deterioration of $20 billion per month is visible; i.e. a deterioration of $240 billion a year. Suddenly, the story of global imbalances righting themselves came under question. The present US run rate is around $40 billion a month or $0.5 trillion a year.

Alongside this, we have news that the Chinese reserves rose by $194 billion in Q3 2010. The Chinese seem to have also passed on some of their problems of exchange rate pegging upon their neighbours by purchasing Japanese, South Korean and Indonesian assets. I am not aware of such behaviour having been observed prior to this in human history. Japan, South Korea and Indonesia have taken unkindly to this behaviour. Given the opacity of the Chinese regime, one can't help wonder if similar things are going on through less visible channels - e.g. a Chinese sovereign wealth fund buys $10 billion of OTC derivatives on Nifty.

So we seem to be headed for quite some escalation of conflict over the Chinese exchange rate regime. Here are some interesting readings on the subject:

- What happens if the RMB is forced to revalue? by Michael Pettis on his blog.

- Why America is going to win the global currency battle, by Martin Wolf in the Financial Times.

- The final end of Bretton Woods 2? on Tim Duy's Fed Watch (the source of the above graph).

- The effect of RMB appreciation on the US-China trade balance, by William Thorbecke on voxEU.

- An interview with Raghuram Rajan on der Spiegel.

- Evolution of the exchange rate regime in Asia.

- How to avoid trade war: A reciprocity requirement, by Daniel Gros on voxEU, which makes a lot of sense to me as one of the least troublesome policy avenues to go down.

Movement on FSDC

MoF press release on FSDC.

For the background on FSDC, see: the budget announcement of Feb 2010, a newspaper column of mine on 16 March, and a collection of responses in the media on 20 March.

- Does the FSDC amount to clipping RBI's wings?

- The FSDC is only a committee. It is not backed by law. So nothing changes about RBI's role and function.

- RBI staff have done speeches saying that financial stability is their job.

- The RBI Act does not contain the word `financial stability'. So while some in RBI might aspire to such a function, the present role and function of the RBI does not include financial stability.

- The FSDC is not a new law, it's merely a committee, so what changes? We already had the HLCC. What changes with the FSDC?

- The FSDC is intended to have a full-time technical secretariat which will work on the problems of financial stability and development. This is something the HLCC lacked. And, the HLCC was chaired by the RBI Governor. He was unable to resolve three classes of situations: (a) Differences between two financial agencies such as the ULIPs question, (b) Differences between two financial agencies when one of them was RBI and (c) Problems of financial stability which require system thinking, which no one Indian agency is good at understanding, given the silo system that is in place. The FSDC should fare better on all three fronts by virtue of being chaired by the finance minister (and backed by a strong secretariat).

- So will the FSDC help matters?

- It all depends on the staff quality that DEA is able to put into it. The "strong secretariat" is only an aspiration at the present moment.

- What is the right role for autonomy for an agency external to MoF?

- There are two clear areas where autonomy is required. The first is about specific transactions. As examples, what entities get bank licenses or exchange licenses? Or, when RBI/SEBI investigate Bank of Rajasthan or MCX-SX. It is highly desirable for MoF to be completely hands-off on these kinds of activities of agencies external to MoF. The second is about monetary policy, i.e. the setting of the short-term interest rate. For these two areas, there is a strong and clear case for de-politicisation and autonomy. In other questions, the case for autonomy is not clear-cut.

- So is it okay for MoF to meddle in the decisions of an external financial agency on subjects like the policy framework for exchange ownership, or the rules about private bank entry?

- The staff quality that DEA is able to put into these functions is supremely important. It is possible to do this right.

- Is FSDC opening a Pandora's box by asking too much of DEA staff quality?

- I think it is an attempt in the right direction. Largely speaking,

it is converting the existing de facto arrangements

into de jure with greater formal structure. If FSDC builds up

top quality staff, then it will make progress. Else, it will be

irrelevant and the present will continue mostly unchanged.

There will of course be ups and downs, but when I look back at the brainpower at DEA from 1993 onwards I feel optimistic about the expected value of FSDC.

The attempt at building a team which works on financial stability and development is an important and a good one. Success on putting together a top quality team cannot be taken for granted. But at the same time, if MoF had not tried this, there would have been a certainty that such a team would not have come together. It is possible to spin this in a gloomy way, but an oversupply of cynicism can crowd out attempts at progress.

Monday, October 11, 2010

Interesting readings

C. J. Chivers has a story in the New York Times from Uzbekistan which links up to an idea that I have often thought would be a great step forward for India: the interior of every police station in the country should be blanketed with video cameras giving feeds out to the Net. As Robert Kaplan says, underdevelopment is where the police are more dangerous than the criminals. If we think surveillance cameras are important in public places, they are triply important to watch the interiors of police stations. On a related note, see this harrowing story about a journalist in Pakistan. Do we do similarly?

A fascinating fact about insurgencies: while a diverse array of weapons can be in fray, ammunition is quite well standardised. Writing about the guns used by the Taliban, C. J. Chivers points out on the New York Times blog, `for the 24 rifles and machine guns in the locker, produced in multiple nations over many decades, only three types of cartridges are required to feed them'.

Shobhana Subramanian in the Financial Express on C. B. Bhave. And, Sandeep Singh has a story in the Hindustan Times about Mr. Bhave coming through fine on one attack on him.

Ashok Desai reviews a book in Business World. Also see.

Auditor and Audit Committee Independence in India by Jayati Sarkar and Subrata Sarkar.

Developments on MCX:

- John J. Lothian is a respected observer of the global securities business. He has written a piece about Financial Technologies Group titled You gotta earn it.

- Mobis Philipose in Mint.

- Deepshikha Sikarwar in the Economic Times.

- A story by Deepika D. Thapliyal on NDTV.

An editorial in Business World on the MoF Working Group on Foreign Investment.

Learn R in Bombay.

Gautam Bhardwaj in the Indian Express on using the NPS to solve the problems of EPFO.

Sunil Jain on the difficulties of the data reported by the Indian statistical system.

An editorial in the Business Standard about developments on private container train companies, which reminds me of the conflicts between DoT and private telecom companies in the early 1990s.

Mobis Philipose worries about the apparent turnover numbers that we're seeing.

An editorial in the Mint on the latest attempt to keep FMC separate from mainstream financial regulation.

Jan Sjunnesson Rao in Education World on the damage that the Right to Education Act is causing.

The Economics of Foodgrain Management in India by Kaushik Basu, DEA Working Paper, September 2010.

A recent paper by Guido Heineck and Bernd Sussmuth finds that the blight of communism runs deep: Using data from the German Socio-Economic Panel, we find that despite twenty years of reunification East Germans are still characterized by a persistent level of social distrust. In comparison to West Germans, they are also less inclined to see others as fair or helpful..

A great interview with Condoleezza Rice on Spiegel Online about the halcyon days of 1989.

The last practical connection with World War I just died away. The legacy of that war, of course, remains with us; everything that came after was attenuated.

David Sanger in the New York Times; Jaswant Singh and Jeffrey N. Wasserstrom on Project Syndicate, on Engaging China. Also see these threats being made against Norway.

Mick Meenan in the New York Times about kabbadi going places.

A great story about the innovative logistics of the Italian army in Ethiopia in 1938.

Greg Mankiw on the high marginal tax rates which are hobbling labour supply in many countries.

China's Charter 08 is a brilliant and well-crafted document, worthy of a Nobel Peace Prize.

Norman MacLean wrote a great article in Lapham's Quarterly about his 1928 experiences with violinist, watercolorist, chess player, and physicist: Albert Michelson. They don't make men like that these days.

Randall Stross in the New York Times on the making of Steve Jobs.

Brad DeLong on Who can replace Larry Summers?.

A great article by Michael Heilemann on binarybonsai: George Lucas Stole Chewbacca, But It's Okay, which made me think about how copyright, patents and `intellectual property' fit uneasily into the creative process. As he says: Chewbacca didn't spring to life out of nowhere, fully formed when Lucas saw his dog in the passenger seat of his car. That's the soundbite. A single step. The reality is complex and human. From vague names floating around, the kernel of an idea, changing purposes and roles of characters, major restructuring, the design hopping from person to person, scrapping the existing concept and going down a different path, seeing existing things in a different light and having to conform a range of ideas to complement and enrich one another.. Everything is a remix.

At the frontiers of computing is `cloud computing', where users rent equipment, e.g. by the hour. Amazon's tariff card for such rental is bad news for developers who built knowledge on Microsoft technologies.

John Taylor has a story about Japanese currency manipulation. Recent research shows that the role of the Yen in global currency arrangements has been waning, and this episode of currency trading by the BoJ will exacerbate this trend.

A fascinating fact about insurgencies: while a diverse array of weapons can be in fray, ammunition is quite well standardised. Writing about the guns used by the Taliban, C. J. Chivers points out on the New York Times blog, `for the 24 rifles and machine guns in the locker, produced in multiple nations over many decades, only three types of cartridges are required to feed them'.

Shobhana Subramanian in the Financial Express on C. B. Bhave. And, Sandeep Singh has a story in the Hindustan Times about Mr. Bhave coming through fine on one attack on him.

Ashok Desai reviews a book in Business World. Also see.

Auditor and Audit Committee Independence in India by Jayati Sarkar and Subrata Sarkar.

Developments on MCX:

- John J. Lothian is a respected observer of the global securities business. He has written a piece about Financial Technologies Group titled You gotta earn it.

- Mobis Philipose in Mint.

- Deepshikha Sikarwar in the Economic Times.

- A story by Deepika D. Thapliyal on NDTV.

An editorial in Business World on the MoF Working Group on Foreign Investment.

Learn R in Bombay.

Gautam Bhardwaj in the Indian Express on using the NPS to solve the problems of EPFO.

Sunil Jain on the difficulties of the data reported by the Indian statistical system.

An editorial in the Business Standard about developments on private container train companies, which reminds me of the conflicts between DoT and private telecom companies in the early 1990s.

Mobis Philipose worries about the apparent turnover numbers that we're seeing.

An editorial in the Mint on the latest attempt to keep FMC separate from mainstream financial regulation.

Jan Sjunnesson Rao in Education World on the damage that the Right to Education Act is causing.

The Economics of Foodgrain Management in India by Kaushik Basu, DEA Working Paper, September 2010.

A recent paper by Guido Heineck and Bernd Sussmuth finds that the blight of communism runs deep: Using data from the German Socio-Economic Panel, we find that despite twenty years of reunification East Germans are still characterized by a persistent level of social distrust. In comparison to West Germans, they are also less inclined to see others as fair or helpful..

A great interview with Condoleezza Rice on Spiegel Online about the halcyon days of 1989.

The last practical connection with World War I just died away. The legacy of that war, of course, remains with us; everything that came after was attenuated.

David Sanger in the New York Times; Jaswant Singh and Jeffrey N. Wasserstrom on Project Syndicate, on Engaging China. Also see these threats being made against Norway.

Mick Meenan in the New York Times about kabbadi going places.

A great story about the innovative logistics of the Italian army in Ethiopia in 1938.

Greg Mankiw on the high marginal tax rates which are hobbling labour supply in many countries.

China's Charter 08 is a brilliant and well-crafted document, worthy of a Nobel Peace Prize.

Norman MacLean wrote a great article in Lapham's Quarterly about his 1928 experiences with violinist, watercolorist, chess player, and physicist: Albert Michelson. They don't make men like that these days.

Randall Stross in the New York Times on the making of Steve Jobs.

Brad DeLong on Who can replace Larry Summers?.

A great article by Michael Heilemann on binarybonsai: George Lucas Stole Chewbacca, But It's Okay, which made me think about how copyright, patents and `intellectual property' fit uneasily into the creative process. As he says: Chewbacca didn't spring to life out of nowhere, fully formed when Lucas saw his dog in the passenger seat of his car. That's the soundbite. A single step. The reality is complex and human. From vague names floating around, the kernel of an idea, changing purposes and roles of characters, major restructuring, the design hopping from person to person, scrapping the existing concept and going down a different path, seeing existing things in a different light and having to conform a range of ideas to complement and enrich one another.. Everything is a remix.

At the frontiers of computing is `cloud computing', where users rent equipment, e.g. by the hour. Amazon's tariff card for such rental is bad news for developers who built knowledge on Microsoft technologies.

John Taylor has a story about Japanese currency manipulation. Recent research shows that the role of the Yen in global currency arrangements has been waning, and this episode of currency trading by the BoJ will exacerbate this trend.

Sunday, October 10, 2010

Interesting ideas in trade

by Ajay Shah.

Akbar's transport of ice

In the ferocious height of the Delhi summer, Akbar setup a mechanism whereby horses started out with ice in Kashmir and rode south. The ice was handed from one horse to another, keeping it constantly on the move. In the end, what reached him was a few kilos of ice.

(I'm unable to recollect where I read this, and google doesn't seem to have heard about it. Please do tell me if you know something about this.)

The Indian ice trade

In 1833, merchants figured out that it was profitable to transport ice from the US to India. The existing technical skills enabled the production of low-grade ice in Calcutta for six weeks of the year at a price of 4p per pound. Transport by sea made possible perfect Boston ice, available round the year, at a price of 3p per pound. Ships would start out with 150 tons of ice and reach Calcutta with 2 tons of ice.

`Ice houses' were built to store ice. The ice houses in Bombay and Calcutta no longer exist, but the ice house in Madras, built in 1841, still exists [location].

In 1878, manufacturing of ice began with the formation of the Bengal Ice Company, and this transport of ice from America dwindled away. By 1882 -- a short four years later -- it had ended. In 1904, there was an ice plant in Peshawar.

Sources: Better than Hooghly slush by Jayakrishnan Nair, in Pragati, June 2010.

The world's largest refinery on the coast of Jamnagar

India's biggest company, Reliance Industries, runs the world's largest refinery off the coast of Jamnagar. Crude oil is imported here, products are made, and re-exported. Here's my interpretation of what's going on. The natural place to put a refinery is in the Persian Gulf, but the political risk in that region is too great, given that the fixed assets in question amount to Rs.2.3 trillion.

What's the most efficient way out? To transport crude oil on the shortest possible hop from the Middle East to a place with political stability. That takes you to the coast of Gujarat.

A new trade: Alaskan water

I just read a story by Sambit Saha in the Telegraph about a new frontier in trade. A firm named True Alaska Bottling has obtained rights to transport 11.34 billion litres of water (i.e. 11.34 million tonnes) out of a lake in Sitka, Alaska. This will be transported to a plant near Bombay, which will be run by a firm named S2C Global, thus yielding bottled water to be sold in India and in the Middle East.

This seems to me to reflect an extension of the themes above. If you want to deliver product into the Middle East, it is better to build a factory in India given political stability and low labour cost. In this sense, it's a bit like Reliance. And, it reminds me of the old ice trade; except that this time we're transporting water.

Thursday, October 07, 2010

Transactions between banks in bad assets: An interesting legal drama

by Pratik Datta and Shubho Roy.

The much awaited decision of the Supreme Court in the matter of ICICI v. Official Liquidator of A.P.S. Star Industries is now available. The case had come as an appeal against a decision of the Gujarat High Court which invalidated transfer of Non-Performing Assets between banks. The decisions of the High Court and the Supreme Court are important in illuminating the legal foundations of Indian finance.

Various borrowers owed a total of Rs. 52.45 crores to ICICI (Amongst which one of the borrowers was M/s A.P.S. Industries). These loans were classified as Non-Performing Assets (NPAs) by ICICI. ICICI transferred these NPAs to Kotak Mahindra on "as is where is" basis by way of a Deed of Assignment. Consequently, the Kotak Mahindra became the full and absolute owner of the debts and as such the entity legally entitled to receive the repayments of debts.

M/s A.P.S. Star Industries subsequently went into liquidation. Kotak Mahindra filed a Company Application in the winding up proceedings of A.P.S. Star, praying for being substituted in the place of ICICI (As it was now the owner of the debt). Though the transfer document between ICICI and Kotak was held to be valid the company court held that such transfers of NPAs was not allowed under the Banking Regulation Act of 1949 (BR Act).

On appeal a Division Bench of the Gujarat High Court upheld the observation of the Company Court on the following main grounds:

To much relief of the banks, the Apex Court has set aside the impugned judgment and order, laying down the following important legal propositions:

While the judgment seems to set law in the correct direction, it raises other questions. The borrowers had argued that the only legal way of transferring financial assets is under Section 5 of the SARFAESI Act which reads:

However, Chief Justice Kapadia, while writing the judgment observed in ¶ 21 that `the SARFESI Act 2002 was enacted enabling specified SPVs to buy the NPAs from the banks'. As discussed, this statement seems to be missing out that even good debts which are not NPAs can be bought by those SPVs under s. 5 of the SARFESI Act. May be this is an inadvertent omission, but it is interesting to observe that Justice Kapadia previously also in Transcore v. Union of India (2008) 1 SCC 125 observed (in ¶ 20) that `it is only when these assets in the hands of the bank/FI becomes sub-standard, doubtful or loss then the account or asset becomes classifiable as a NPA and it is only then that the NPA Act comes into operation'. The same is reiterated in ¶ 30. Clearly, these observations do not quite fit with the literal interpretation of s. 5. Probably the pedantic have got another question lingering in their minds: `Can a bank/financial institution sell off a debt, which is not a NPA, to a securitisation/assets reconstruction company?'

One also asks what remains of Section 6 of the BR Act which describes what activities banks can take part in. Justice Kapadia states `In other words, the 1949 Act allows banking companies to undertake activities and businesses as long as they do not attract prohibitions and restrictions like those contained in Sections 8 and 9'. This would mean that while the legislature drafted Section 6, this is irrelevant today. He also goes on to state `Thus, RBI is empowered to enact a policy which would enable banking companies to engage in activities in addition to core banking process it defines as to what constitutes ``banking business''.'

This implies that there is unfettered power with RBI to define what business banks can take part in. This is unusual as it seems that there are no parliamentary control over what banking business can imply. Unlike `securities' which is defined under the Securities Contract Regulation Act by Parliament and only the central government may modify it by notification, (and therefore no regulator is free to define any instrument as a security and regulate it) `banking' seems to be under a Henry VII clause for RBI. There seems to be no provision under the BR Act allowing the central government (let alone the RBI) to change the definition of `banking'. The judgment however empowers RBI to do so without and rider or guidelines. This also goes against the principles of interpreting laws as it makes all provisions in Section 6(a) to (o) irrelevant.

The judgment reveals the state of financial laws in the country which are unable to guide the judiciary unambiguously. The judicial interpretations also seem to alter the nature of the laws and the drift between the letter of the law and its meaning continues to increase.

The much awaited decision of the Supreme Court in the matter of ICICI v. Official Liquidator of A.P.S. Star Industries is now available. The case had come as an appeal against a decision of the Gujarat High Court which invalidated transfer of Non-Performing Assets between banks. The decisions of the High Court and the Supreme Court are important in illuminating the legal foundations of Indian finance.

Background

Various borrowers owed a total of Rs. 52.45 crores to ICICI (Amongst which one of the borrowers was M/s A.P.S. Industries). These loans were classified as Non-Performing Assets (NPAs) by ICICI. ICICI transferred these NPAs to Kotak Mahindra on "as is where is" basis by way of a Deed of Assignment. Consequently, the Kotak Mahindra became the full and absolute owner of the debts and as such the entity legally entitled to receive the repayments of debts.

M/s A.P.S. Star Industries subsequently went into liquidation. Kotak Mahindra filed a Company Application in the winding up proceedings of A.P.S. Star, praying for being substituted in the place of ICICI (As it was now the owner of the debt). Though the transfer document between ICICI and Kotak was held to be valid the company court held that such transfers of NPAs was not allowed under the Banking Regulation Act of 1949 (BR Act).

The High Court ruling

On appeal a Division Bench of the Gujarat High Court upheld the observation of the Company Court on the following main grounds:

- Section 6 of BR Act gives and exhaustive list of activities a bank is allowed to carry out and sale of NPAs is not present in the list.

- Since banks prohibited from trading activities (See section 8 of the BR Act) and the sale of NPAs is essentially trading, such transfer was invalid.

- Such trading of NPAs would mean transfer of NPA from one banks balance sheet to another without any resolution and therefore against the health of the banking industry.

- Since individual loans were lumped together and bought there was no way to ascertain the value of individual loans and the amount recovered from them. This made such loans essentially speculative trading.

- Since the customer is forced to transact with another bank now and also he is being lumped with other loans, this amounts to violation of the relationship between the bank and the customer.

- By legislating s.5 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act), the Parliament has made it clear that only securitisation companies can buy NPAs and not banks.

The Supreme Court ruling

To much relief of the banks, the Apex Court has set aside the impugned judgment and order, laying down the following important legal propositions:

- Section 6(1) of the BR Act is a general provision and enumerates topics as fields in which banks can carry on their business. This is the core banking business. However, RBI, being the regulator, under Section 21 and 35A can issue directions having statutory force, laying down parameters enabling banks to expand their business. Such parameters will define `banking business'. (¶ 13)

- RBI, by issuing guidelines authorized banks to deal in NPAs and such guidelines cannot be held ultra vires of the Act. Such guidelines have statutory force and hence inter se transfer of NPAs between banks is permissible. (¶ 14)

- The 2005 guidelines of RBI are not to eliminate NPAs but to restructure the same. Such restructuring cannot be treated as trading. (¶ 15)

- The SARFAESI Act was enacted enabling specified SPVs to buy the NPAs from the banks. However, from that it does not follow that banks cannot transfer their own assets. (¶ 21)

Deeper issues

While the judgment seems to set law in the correct direction, it raises other questions. The borrowers had argued that the only legal way of transferring financial assets is under Section 5 of the SARFAESI Act which reads:

``Notwithstanding anything contained in any agreement or any other law for the time being in force, any securitisation company or reconstruction company may acquire financial assets of any bank/FI..''

However, Chief Justice Kapadia, while writing the judgment observed in ¶ 21 that `the SARFESI Act 2002 was enacted enabling specified SPVs to buy the NPAs from the banks'. As discussed, this statement seems to be missing out that even good debts which are not NPAs can be bought by those SPVs under s. 5 of the SARFESI Act. May be this is an inadvertent omission, but it is interesting to observe that Justice Kapadia previously also in Transcore v. Union of India (2008) 1 SCC 125 observed (in ¶ 20) that `it is only when these assets in the hands of the bank/FI becomes sub-standard, doubtful or loss then the account or asset becomes classifiable as a NPA and it is only then that the NPA Act comes into operation'. The same is reiterated in ¶ 30. Clearly, these observations do not quite fit with the literal interpretation of s. 5. Probably the pedantic have got another question lingering in their minds: `Can a bank/financial institution sell off a debt, which is not a NPA, to a securitisation/assets reconstruction company?'

One also asks what remains of Section 6 of the BR Act which describes what activities banks can take part in. Justice Kapadia states `In other words, the 1949 Act allows banking companies to undertake activities and businesses as long as they do not attract prohibitions and restrictions like those contained in Sections 8 and 9'. This would mean that while the legislature drafted Section 6, this is irrelevant today. He also goes on to state `Thus, RBI is empowered to enact a policy which would enable banking companies to engage in activities in addition to core banking process it defines as to what constitutes ``banking business''.'

This implies that there is unfettered power with RBI to define what business banks can take part in. This is unusual as it seems that there are no parliamentary control over what banking business can imply. Unlike `securities' which is defined under the Securities Contract Regulation Act by Parliament and only the central government may modify it by notification, (and therefore no regulator is free to define any instrument as a security and regulate it) `banking' seems to be under a Henry VII clause for RBI. There seems to be no provision under the BR Act allowing the central government (let alone the RBI) to change the definition of `banking'. The judgment however empowers RBI to do so without and rider or guidelines. This also goes against the principles of interpreting laws as it makes all provisions in Section 6(a) to (o) irrelevant.

Conclusion

Wednesday, October 06, 2010

Is there a problem with rupee appreciation?

There is a lot of talk about capital inflows, rupee appreciation, concerns about export competitiveness, etc. It made me pull up the data to look at what is going on. The graph shows the nominal and real effective exchange rate of the rupee. The source is the BIS: the best computation of these indexes presently available.

There is one constraint of this data: it ends in August. The picture shown there is rather benign. Over the five year period shown in the graph, modest REER fluctuations are visible. Over the recent period of roughly a year, where RBI intervention has subsided, it isn't clear that something dramatic shifted.

And, I like to always remind everyone that the REER is a rather weak way to think about export competitiveness, so even if there was a sharp rise in the REER, we'd have to be cautious in rushing to conclusions about what it is saying.

The people making the case for currency trading by RBI have to cross four hurdles:

|

| Real and Nominal effective exchange rate of the Indian Rupee |

There is one constraint of this data: it ends in August. The picture shown there is rather benign. Over the five year period shown in the graph, modest REER fluctuations are visible. Over the recent period of roughly a year, where RBI intervention has subsided, it isn't clear that something dramatic shifted.

And, I like to always remind everyone that the REER is a rather weak way to think about export competitiveness, so even if there was a sharp rise in the REER, we'd have to be cautious in rushing to conclusions about what it is saying.

The people making the case for currency trading by RBI have to cross four hurdles:

- Is there a crisis on export competitiveness that is rooted in exchange rate misalignment?

- How can controlling nominal things (the exchange rate) influence real things (the real rate)?

- Given a choice of using the tool of monetary policy for the purpose of delivering low and stable inflation (which benefits every citizen of India), versus the purpose of delivering some modification of the nominal exchange rate (which benefits a sectarian interest at best), what is the best choice?

- How can RBI be held accountable to maximise the interests of the people of India, if it is to do active trading on the currency market? What checks and balances, and what accountability mechanisms, need to be put into place in order to run a trading room in the government sector?

It is not so long ago (until early 2007) that RBI was actively trading in the currency market, championing the cause of India's exporters, and we saw how much trouble it got them in. In some ways, our inflation crisis today is the legacy of the unprecedented credit boom of the Y V Reddy years. Today's India is only more open than the India where Y V Reddy's regime tripped up on currency trading, so the challenges in embarking on that path today are even more daunting.

Friday, October 01, 2010

Signs of life in stock lending

I wrote a column in the Financial Express today about the first signs of life in stock lending. This is one of the last building blocks of the ecosystem of the equity market.

Also see: Mobis Philipose in Mint on 13 September.

Also see: Mobis Philipose in Mint on 13 September.

Subscribe to:

Posts (Atom)