by Surya Prakash B S and Kangan Upadhye.

Is it possible to have a unified view of a legislation that pieces together its various provisions? In our paper we present a novel methodology that measures direct tax provisions of the Finance Bill, 2017 (Government of India Budget, 2017) presented by the Union Government of India to the Lok Sabha, against accepted principles of taxation and tax system design.

The Finance Bill seeks to amend many parts of the Income Tax Act and consequently impacts sections of the society differently. Popular media coverage tends to focus on impact on some sectors or a few controversial measures. This is natural given that budget making is a contentious exercise that needs to address concerns from all quarters. Our methodology avoids analysis either from the perspective of the state (revenue mobilisation) or the taxpayers (revenue minimisation). It measures each direct tax provision to see how well they perform against principles of taxation.

Our method consists of a set of “attributes” and “impacts” for which we assign scores. Attributes relate to the objective features of the provisions: we categorise provisions/amendments into compliance, substantive, procedural, exemptions, collection and recovery, anti-avoidance, penal provisions, international taxation and adjudication machinery. A total of 97 provisions in the Finance Bill 2017 are categorised under these attributes. A single provision could have more than one attribute. For example, the amendments proposed to section 13A which is related to exemption from paying income-tax for political parties, to discourage the cash transactions and to bring transparency about funding political parties is an example of a provision categorised under more than one attribute. It is categorised not only under compliance but also recognised as substantive.

A summary of the above step is depicted below. It can be observed that the Finance Bill, 2017 contained 26 provisions relating to ‘Exemptions’, 22 that were ‘Substantive’ and 21 that made changes to ‘Computation’.

Since the provisions could have various levels of impact, we go on to score them on a seven point scale (-3 to +3) against each of the following seven principles of an ideal tax system design:

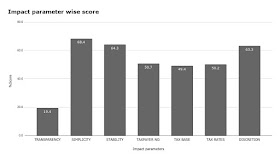

The scores are calculated in percentage terms (after converting negative scores to positive for ease of comparison) and the results are as depicted in the figure below.

The provisions in the bill score fairly well on simplicity, stability and discretion parameters with moderate scores on taxpayers, tax base and rates relative to the others. The provisions perform poorly on the transparency parameter.

Our results from the framework do support the popular thinking about the 2017 financial bill the way industry experts and practitioners have interpreted in the budget discourse (Chakrabarti et al. 2017). For example, the amendment to section 132 which empowers relevant authorities under the Income Tax Act, 1961 to carry out a search or seizure without having to declare reason to believe such person or any authority or appellate tribunal, previously required under section 132 of the Income Tax Act, 1961 (Government of India Budget, 2017).

The earlier provisions empowered authorities to enter and search any building, person if they had a reason to believe that the person had failed to disclose material facts. As critics argue without having a reason to declare for search or seizure this power can be misused to conduct arbitrary investigations leading to harrassments and tax terrorism. This provision was rated low on all the parameters. By adopting such a systematic approach to evaluating tax amendments, this could serve as an evidence informed input to the design of taxes in our budgeting system.

To the best of our knowledge, we have not come across any similar methodology in use in any major economy. The methodology is objective, the impact parameters and the attributes categorised are transparent, and these assumptions can be revised by those that seek to view the results based on alternate views or perform a sensitivity analysis.

We are aware that scores given can be made more accurate through data based post hoc impact assessments. Further research is required on this aspect.

The practical value of the results from our approach are many. It would a) enable us to base the study of the Finance Acts against principles of a good tax system b) provide a comprehensive view of the taxation system rather than a view traditionally restricted to revenue objectives or taxpayer hardship; and c) enable a mapping of the trajectory of tax policy by allowing us to compare across years. It can be viewed as a first step towards making the budget-making process transparent, empirical, and inclusive. The methodology used in this paper can potentially also be used to study other legislation and amendments.

Is it possible to have a unified view of a legislation that pieces together its various provisions? In our paper we present a novel methodology that measures direct tax provisions of the Finance Bill, 2017 (Government of India Budget, 2017) presented by the Union Government of India to the Lok Sabha, against accepted principles of taxation and tax system design.

The Finance Bill seeks to amend many parts of the Income Tax Act and consequently impacts sections of the society differently. Popular media coverage tends to focus on impact on some sectors or a few controversial measures. This is natural given that budget making is a contentious exercise that needs to address concerns from all quarters. Our methodology avoids analysis either from the perspective of the state (revenue mobilisation) or the taxpayers (revenue minimisation). It measures each direct tax provision to see how well they perform against principles of taxation.

Our method consists of a set of “attributes” and “impacts” for which we assign scores. Attributes relate to the objective features of the provisions: we categorise provisions/amendments into compliance, substantive, procedural, exemptions, collection and recovery, anti-avoidance, penal provisions, international taxation and adjudication machinery. A total of 97 provisions in the Finance Bill 2017 are categorised under these attributes. A single provision could have more than one attribute. For example, the amendments proposed to section 13A which is related to exemption from paying income-tax for political parties, to discourage the cash transactions and to bring transparency about funding political parties is an example of a provision categorised under more than one attribute. It is categorised not only under compliance but also recognised as substantive.

A summary of the above step is depicted below. It can be observed that the Finance Bill, 2017 contained 26 provisions relating to ‘Exemptions’, 22 that were ‘Substantive’ and 21 that made changes to ‘Computation’.

Since the provisions could have various levels of impact, we go on to score them on a seven point scale (-3 to +3) against each of the following seven principles of an ideal tax system design:

- Transparency: Whether there have been any prior public consultations.

- Simplicity: Whether the provisions makes levy and collection simpler.

- Stability: Whether the provisions are prospective or retrospective in nature.

- Discretionary power: Whether and to what extent discretionary power of tax officers have been enhanced or decreased.

- Tax rates: Whether and by how much have tax rates have been decreased. Lowering tax rates get higher scores.

- Tax base: Is the income on which tax is levied increased or decreased. As a principle when more types of income are charged, a higher score is given. As a corollary, exemptions are scored lower.

- Number of taxpayers: Provisions that extend the levy to more taxpayers have higher score. If a few of them are exempted it gets a lower score.

The scores are calculated in percentage terms (after converting negative scores to positive for ease of comparison) and the results are as depicted in the figure below.

The provisions in the bill score fairly well on simplicity, stability and discretion parameters with moderate scores on taxpayers, tax base and rates relative to the others. The provisions perform poorly on the transparency parameter.

Our results from the framework do support the popular thinking about the 2017 financial bill the way industry experts and practitioners have interpreted in the budget discourse (Chakrabarti et al. 2017). For example, the amendment to section 132 which empowers relevant authorities under the Income Tax Act, 1961 to carry out a search or seizure without having to declare reason to believe such person or any authority or appellate tribunal, previously required under section 132 of the Income Tax Act, 1961 (Government of India Budget, 2017).

The earlier provisions empowered authorities to enter and search any building, person if they had a reason to believe that the person had failed to disclose material facts. As critics argue without having a reason to declare for search or seizure this power can be misused to conduct arbitrary investigations leading to harrassments and tax terrorism. This provision was rated low on all the parameters. By adopting such a systematic approach to evaluating tax amendments, this could serve as an evidence informed input to the design of taxes in our budgeting system.

To the best of our knowledge, we have not come across any similar methodology in use in any major economy. The methodology is objective, the impact parameters and the attributes categorised are transparent, and these assumptions can be revised by those that seek to view the results based on alternate views or perform a sensitivity analysis.

We are aware that scores given can be made more accurate through data based post hoc impact assessments. Further research is required on this aspect.

The practical value of the results from our approach are many. It would a) enable us to base the study of the Finance Acts against principles of a good tax system b) provide a comprehensive view of the taxation system rather than a view traditionally restricted to revenue objectives or taxpayer hardship; and c) enable a mapping of the trajectory of tax policy by allowing us to compare across years. It can be viewed as a first step towards making the budget-making process transparent, empirical, and inclusive. The methodology used in this paper can potentially also be used to study other legislation and amendments.

The authors are researchers at Daksh. The authors are thankful to Shreya Rao and Shweta Mallya for their contribution during the conceptualisation phase of this paper. This paper was presented at the APU-NIPFP workshop Strengthening the Republic #1, January 11, 2020.

No comments:

Post a Comment

Please note: Comments are moderated. Only civilised conversation is permitted on this blog. Criticism is perfectly okay; uncivilised language is not. We delete any comment which is spam, has personal attacks against anyone, or uses foul language. We delete any comment which does not contribute to the intellectual discussion about the blog article in question.

LaTeX mathematics works. This means that if you want to say $10 you have to say \$10.